Keeping an eye on the Fed’s projections

- 09.15.23

- Markets & Investing

- Commentary

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Rising oil prices are a key risk for the Fed

- Labor market rebalancing is good news for the Fed

- No hike in September, but another hike is still possible

The Energizer Bunny! That’s the term that best describes the U.S. economy. Despite calls for a recession, growth has defied expectations – remaining remarkably resilient thus far this year. While the headwinds to growth (i.e., depleted excess savings, student loan repayments, softening job growth) are building, the economy remains on track for a strong 3Q (Atlanta Fed Q3 GDPNow growth estimate: 4.9%). The latest surge appears to be due to a last burst of pent-up travel demand and soaring manufacturing investment (courtesy of prior stimulus acts). While inflation has eased, the uptick in oil prices (if sustained) could create challenges for the outlook. How will these dynamics shape the Fed’s thinking at the September 19-20 FOMC meeting and impact its updated economic projections? Here are our latest thoughts.

- Keeping an eye on the Fed’s projections | Chair Powell’s Jackson Hole speech did not shed much insight on the direction of policy. Instead, he reiterated what we already know – the Fed is committed to its 2.0% inflation target and the choice between holding rates steady or raising them is ‘data dependent.’ However, since the Fed’s June economic projections, there has been one additional rate hike, upward growth surprises, downward payroll revisions, peak disinflation, rising oil prices, sharply higher interest rates and a buoyant stock market. Below are the potential impacts to the Fed’s updated projections.

- Economic growth | The strength of the economy has likely surprised Fed officials, particularly given the aggressiveness of the tightening cycle over the last 1.5 years. While policymakers lifted their 2023 GDP projection in June from 0.4% to 1.0%, further upward revisions are likely. We expect the Fed to double its 2023’s growth rate to ~2.0%., just as our economist did. In addition, 2024’s growth (+1.1% forecast) will be a primary focus. While we expect growth to slow to 0.4%, it will be telling whether the Fed lowers its estimate as staff economists are no longer forecasting a recession next year.

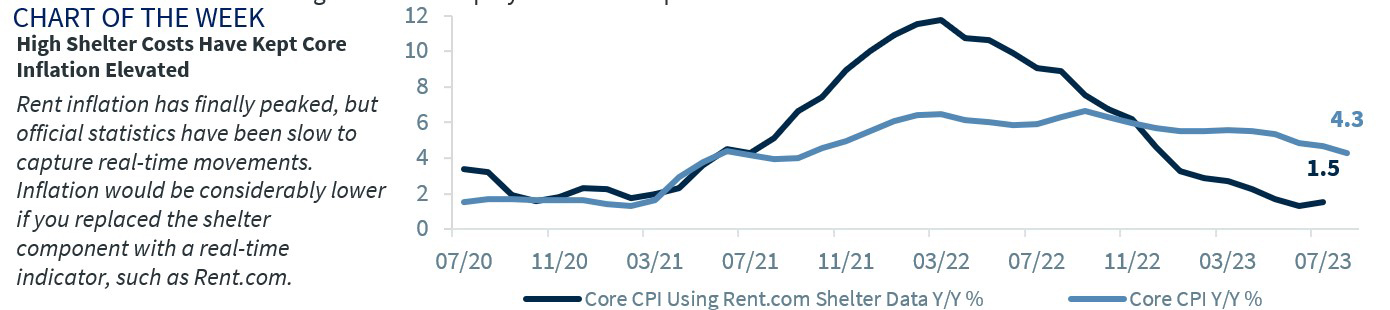

- Inflation | The sharp drop in PCE inflation from a peak of ~7.0% last June to ~3.3% (not far from the Fed’s 3.2% 2023 projection) has been a welcome development. However, the core measure remains stubbornly elevated at 4.3%. While policymakers acknowledge there is substantial disinflation in the pipeline from the lagged pass through of lower rent prices into the inflation calculation, there is considerable uncertainty about how quickly inflation will move back to trend. Fed officials will likely maintain their 2024 (2.5%) and 2025 (2.1%) PCE projections. The biggest risk: the sharp rise in oil prices (~+25+% over the last three months) could drive inflation higher in the near term and potentially spook the Fed.

- Unemployment | The labor market is moving into balance with labor demand softening (i.e., declining JOLTS) and the supply of labor rising (i.e., rising labor force participation rate). These dynamics have pushed the unemployment rate up to 3.8% (for the right reasons) and eased wage pressures (although they are still too high). However, the Fed wants labor rebalancing to continue. No major changes are expected in the Fed’s unemployment projections of 4.1% in 2023 and 4.6% in 2024. Similarly, our economist expects job growth to turn mildly negative in 1Q24 and the unemployment rate to peak near 5% in 1H24.

- Federal funds rate | The ongoing strength in the economy will likely lead the Fed to raise rates one additional time in 2023 to the 5.50% - 5.75% level – similar to the Fed’s 2023 projection of 5.6%. However, what’s more important to the market is where the Fed forecasts rates in 2024 and beyond. In June, the Fed projected nearly 100 bps of rate cuts in 2024, with the fed funds rate falling to 4.6% and a longer-run equilibrium level of 2.5%. We do not expect any major changes to the Fed’s rate projections for 2024 and beyond. Our economist expects the Fed to begin cutting rates in 2H24 as inflation continues to ease. This is consistent with the average time from the end of the tightening cycle to the first cut of seven months. In total, our economist expects the upper limit of the fed funds target range will fall to 4.5% by year-end 2024.

- Bottom line | The Fed will likely remain on hold at the September 19-20 FOMC meeting, with the futures market reflecting a 97% probability of no rate hike. While it is a close call, we expect the Fed to hike one more time before the end of the year, as an insurance policy as growth and inflation remain uncomfortably elevated. But that economic scenario is unlikely to persist as we forecast the disinflationary trend to continue (as decelerating shelter prices take effect) and the economy endures a mild recession beginning in 1Q24. As a result, the Fed is likely to begin cutting interest rates around mid-year. Our hope is that the Fed outlines a similar scenario which should be positive for both the equity and fixed income markets over the next twelve months. If it does not and keeps hiking interest rates higher and longer than we expect, that could lead to a deeper and longer lasting recession. Why? Because we disagree that the US economy has become less interest rate sensitive. A more pronounced downturn would be a negative for the equity market and a positive for the bond market.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.